1. What is the Security and Vulnerability Management Market Overview – definition, scope, and significance?

The Security and Vulnerability Management (SVM) market comprises solutions and services that identify, assess, prioritize, and remediate security weaknesses across IT environments. Its scope spans on‑premise and cloud deployments, covering a range of offerings such as vulnerability scanners, patch management tools, threat intelligence platforms, and managed security services. The market is significant because cyber‑threats continue to evolve, driving organizations to adopt proactive measures that protect data, maintain regulatory compliance, and safeguard business continuity across all industry verticals.

2. What are the primary drivers, restraints, challenges, and opportunities in the Security and Vulnerability Management Market?

Key drivers include rising cyber‑attack sophistication, stringent data‑privacy regulations, and increasing cloud adoption that expands the attack surface. Restraints stem from budget constraints in smaller enterprises and the complexity of integrating legacy systems with modern SVM solutions. Major challenges involve talent shortages in cybersecurity and the rapid pace of vulnerability emergence, which can outstrip remediation capabilities. Opportunities arise from the growing demand for automated, AI‑enhanced vulnerability detection, as well as the expansion of managed security services in emerging markets.

3. Which growth trends are currently shaping the Security and Vulnerability Management Market?

Current trends feature a shift toward cloud‑native vulnerability management, the integration of machine learning for risk prioritization, and the convergence of SVM tools with broader security orchestration, automation, and response (SOAR) platforms. Additionally, the market sees greater adoption of continuous monitoring models and the rise of zero‑trust architectures that embed vulnerability assessments into every access decision.

4. How did COVID‑19 impact the Security and Vulnerability Management Market and what is the recovery trajectory?

The pandemic accelerated digital transformation as organizations rapidly moved workloads to the cloud, exposing new vulnerabilities and increasing demand for SVM solutions. While initial spending was redirected to remote‑work enablement, security budgets rebounded quickly, leading to a sustained upward trajectory. The market is now in a recovery phase characterized by heightened investment in automated remediation and expanded managed services to support distributed workforces.

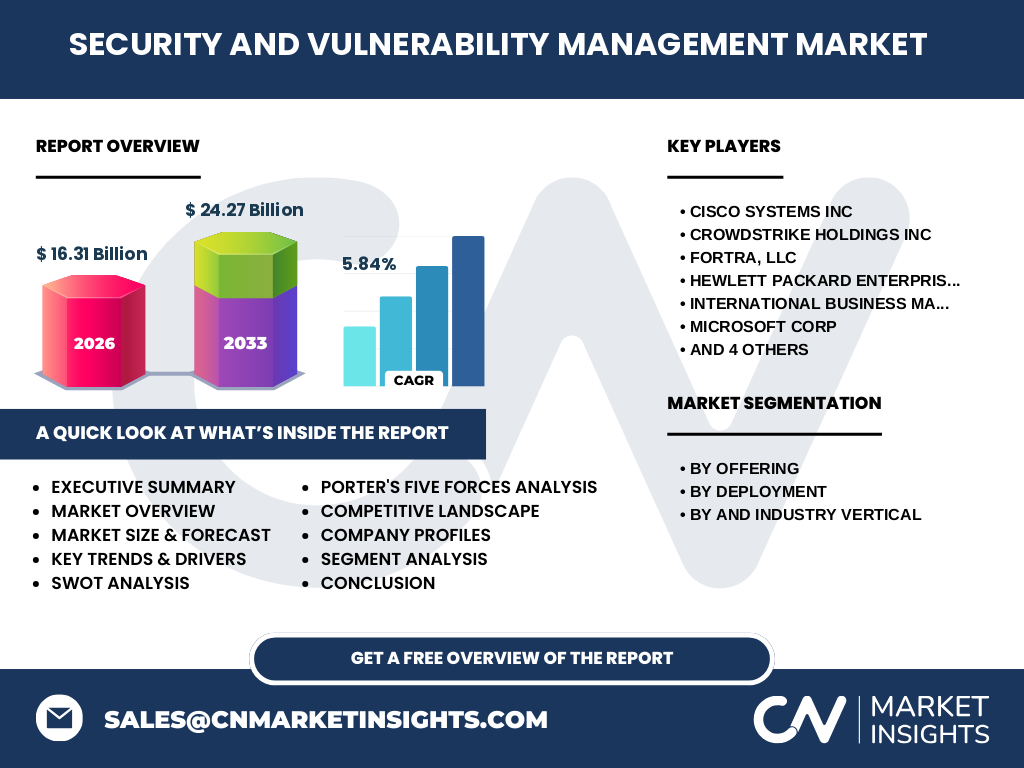

5. Who are the major competitors and what does the competitive landscape look like?

The market is dominated by a mix of legacy vendors and fast‑growing specialist firms. Leading players include Cisco Systems Inc, CrowdStrike Holdings Inc, Fortra, LLC, Hewlett Packard Enterprise Development LP, International Business Machines Corp, Microsoft Corp, Qualys Inc, Rapid, Skybox Security, Inc, and Tenable Holdings Inc. Consolidation activity is moderate, with strategic acquisitions aimed at strengthening AI capabilities and expanding cloud‑based offerings.

6. What are the key findings in the Executive Summary of the Security and Vulnerability Management Market?

The SVM market is projected to grow from a 2026 valuation of $16.31 billion to $24.27 billion by 2033, delivering a CAGR of 5.84 %. Growth is driven by regulatory pressure, cloud migration, and advanced threat landscapes. Solution and service offerings are gaining traction across BFSI, IT & Telecom, Retail & E‑Commerce, Healthcare, and Government & Utilities. Competitive dynamics favor vendors that combine robust detection engines with scalable, automated remediation workflows.

7. What is the forecast for the Security and Vulnerability Management Market for 2025‑2032?

Based on the provided CAGR of 5.84 %, the market will continue a steady expansion through 2032, maintaining double‑digit growth in annual revenues. The forecast anticipates sustained demand for cloud‑based solutions, increased spend on AI‑driven analytics, and a broader adoption of managed vulnerability services, especially in regions where cybersecurity talent is scarce.

8. How is the Security and Vulnerability Management Market sized and shared by segment?

Segmentation is organized by offering, deployment, and industry vertical. Offering‑wise, the market is split between Solution and Service categories, with services capturing a growing share due to managed security trends. Deployment divides into On‑Premise and Cloud, where Cloud is outpacing On‑Premise as enterprises shift workloads. Vertically, the market serves BFSI, IT & Telecom, Retail & E‑Commerce, Healthcare, and Government & Utilities, each requiring tailored compliance and risk‑management capabilities.

9. What is the geographic distribution of the global Security and Vulnerability Management Market?

The market exhibits a worldwide footprint, with North America leading due to early technology adoption and stringent regulatory regimes. Europe follows closely, driven by GDPR compliance, while the APAC region shows rapid growth fueled by expanding digital economies and increasing cyber‑risk awareness. Emerging markets in Latin America and the Middle East contribute incremental demand, primarily through cloud service adoption.

10. What does the regional analysis reveal about market performance?

North America benefits from a mature vendor ecosystem and high cybersecurity spending, resulting in the largest revenue share. Europe’s market is characterized by strong public‑sector investments and cross‑border data‑privacy mandates. APAC’s growth is propelled by large‑scale cloud migration projects in China, India, and Southeast Asia, creating opportunities for both local and global vendors. The Middle East and Africa are emerging as new frontiers, with governments initiating national cyber‑security strategies.

11. Which companies lead the Security and Vulnerability Management Market and what are their strategies?

Key leaders include Cisco, leveraging its networking portfolio to embed vulnerability intelligence across infrastructure; CrowdStrike, focusing on cloud‑native endpoint protection; Tenable, known for comprehensive vulnerability scanning; and Microsoft, integrating SVM capabilities within its Azure and Defender suites. Strategies revolve around expanding AI functionality, forming strategic partnerships, and acquiring niche players to broaden solution breadth.

12. How does Porter’s Five Forces analysis apply to the Security and Vulnerability Management Market?

• Threat of new entrants: Moderate, as high R&D costs and established vendor relationships create barriers. • Bargaining power of buyers: Increasing, due to abundant solution choices and price sensitivity. • Bargaining power of suppliers: Low, because most components are software‑based and can be sourced internally. • Threat of substitutes: Limited, since comprehensive vulnerability management remains a core security requirement. • Rivalry among existing competitors: Intense, driven by rapid innovation cycles and the need to differentiate through AI and managed services.

13. What are the SWOT highlights for the Security and Vulnerability Management Market?

Strengths: Essential role in cyber‑risk mitigation, strong growth outlook, and expanding cloud adoption.

Weaknesses: Integration complexity with legacy environments and talent shortages.

Opportunities: AI‑enhanced analytics, managed service models, and emerging regional markets.

Threats: Constantly evolving threat landscape and potential budgetary pullbacks in economic downturns.

14. How is the value chain structured in the Security and Vulnerability Management Market?

The value chain begins with research & development of detection engines, followed by product design and integration services. Distribution occurs through direct sales, channel partners, and cloud marketplaces. Post‑sale, vendors provide implementation, training, and managed monitoring services, creating recurring revenue streams. End‑users feed threat data back to vendors, completing a feedback loop that drives continuous improvement.

15. What investment insights can be drawn for stakeholders in the Security and Vulnerability Management Market?

Investors should focus on companies that demonstrate strong cloud capabilities, AI‑driven automation, and a growing managed services footprint. Partnerships with cloud platforms and acquisitions that add specialized detection technologies are positive signals. Additionally, firms with diversified vertical coverage reduce exposure to sector‑specific regulatory shocks.

16. What are the concluding takeaways from the Security and Vulnerability Management Market analysis?

The SVM market is on a robust growth path, underscored by a 5.84 % CAGR and a projected size of $24.27 billion by 2033. Cloud migration, regulatory pressure, and sophisticated cyber threats are the primary growth engines. Companies that innovate with AI, expand managed services, and pursue strategic acquisitions are well positioned to capture market share.

17. How was the research for this report conducted?

The study employed a mixed‑methods approach, combining primary interviews with industry experts, secondary data from vendor disclosures, and quantitative analysis of market revenues. Trend extrapolation was based on the provided CAGR, while segmentation analysis used the defined offering, deployment, and vertical categories.

18. What is the scope of this research and its limitations?

The research covers the global Security and Vulnerability Management market, focusing on solution and service offerings across on‑premise and cloud deployments, and five key industry verticals. Limitations include reliance on publicly available financial figures and the absence of granular regional revenue breakdowns beyond the high‑level geographic distribution.

19. Which key companies have recent developments, and what are the notable product launches or partnerships?

Recent highlights include Cisco’s integration of vulnerability insights into its SecureX platform, CrowdStrike’s launch of a cloud‑native threat‑intelligence module, Tenable’s partnership with major cloud providers to deliver continuous assessment, Microsoft’s expansion of Azure Defender for hybrid workloads, and Qualys’s introduction of AI‑based asset prioritization. These developments illustrate the market’s focus on automation, cloud integration, and collaborative ecosystems.